Got a Holiday Bonus? 5 Smart Ways to Invest It for Your Future (Don’t Just Spend It!)

The notification arrives, often with a quiet chime or a bolded line item on your payslip: “Annual Bonus.” It’s a moment of well-earned satisfaction, a tangible reward for a year of hard work. The immediate temptation is powerful—fantasies of lavish dinners, new gadgets, or a spontaneous vacation dance in our minds. But what if this year-end windfall wasn’t just fleeting fun money, but a powerful catalyst for your long-term financial well-being?

That bonus check represents a unique opportunity. Unlike your regular salary, which is often earmarked for recurring expenses, this is a lump sum with untapped potential. Treating it with intention can have a disproportionately large impact on your financial future. This guide moves beyond the simple “save your money” advice, offering a strategic framework to help you decide the smartest way to deploy your bonus, transforming it from a temporary boost into a lasting asset.

The First, Non-Negotiable Priority: Attacking High-Interest Debt

Before we even whisper the word “invest,” we must address the financial equivalent of a boat taking on water: high-interest debt. Think of credit card balances, personal loans, or any debt with an annual percentage rate (APR) in the double digits. Trying to build wealth through investing while carrying this kind of debt is like trying to fill a bucket with a hole in it.

“Think of it this way: paying off a credit card with a 20% APR is the same as earning a guaranteed, tax-free 20% return on your money. No investment in the stock market can reliably offer that.”

The average stock market return, historically, has hovered around 7-10% annually. When you compare that to the 18-25% APR on most credit cards, the math is undeniable. Every dollar you put toward that debt is a dollar that is no longer compounding *against* you. This isn’t just about eliminating a monthly payment; it’s about reclaiming your financial momentum. If you have this type of debt, using your bonus to erase it is almost always the single most powerful financial move you can make. It addresses the core question of investing bonus vs paying off debt head-on.

The 5 Smartest Paths for Your Bonus

Once you’ve addressed any high-interest debt, you can turn your attention to growth. Here are five strategic ways to invest your bonus, each serving a different but vital purpose.

1. Supercharge Your Retirement: The Tax-Smart Move

One of the most efficient ways to deploy your bonus is to channel it into a tax-advantaged retirement account. This is a classic example of making your money work twice as hard.

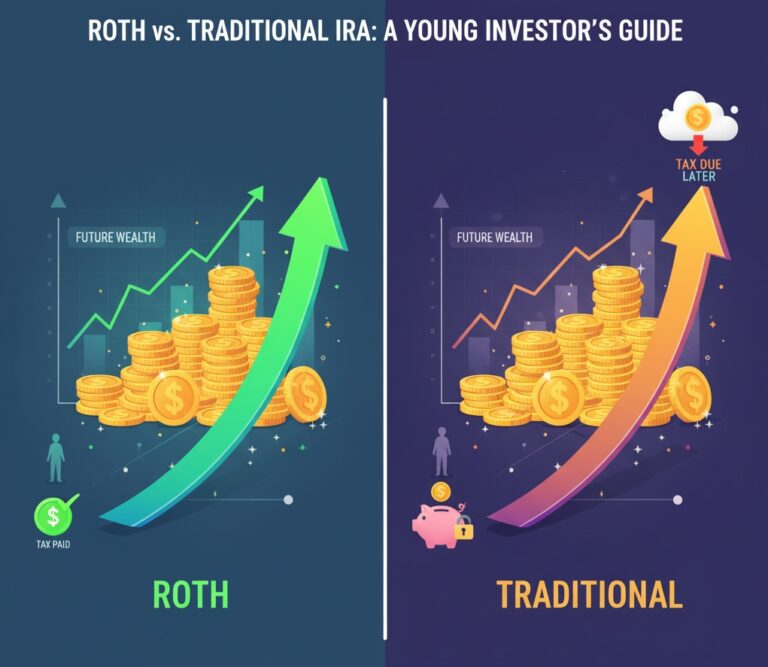

- Traditional IRA/401(k): A contribution here can be tax-deductible, meaning it lowers your taxable income for the year you contribute. It’s like getting an immediate return on your investment from the government. This is a perfect use for an IRA contribution with bonus.

- Roth IRA/401(k): You contribute after-tax dollars, but your investments grow and can be withdrawn completely tax-free in retirement. For a young professional, decades of tax-free growth can be monumental.

Using your bonus to max out your annual contribution is a move your future self will thank you for. It’s a direct investment in your long-term security and a powerful tax-efficient way to invest bonus money.

2. Plant a Money Tree in the Market: The Growth Engine

If your retirement accounts are on track, using your bonus to open or add to a taxable brokerage account is your next frontier. This isn’t about picking the next hot stock. It’s about systematic, long-term growth.

For a lump sum like a bonus, the simplest and often most effective strategy is to invest in a low-cost index fund or ETF (Exchange-Traded Fund). Think of an S&P 500 index fund as buying a tiny slice of America’s 500 largest companies. You get broad diversification instantly, minimizing risk while capturing the overall growth of the market. This is the best way to invest a $5000 bonus for pure, long-term growth.

3. Save for a Major Goal: The Milestone Maker

Not all investments are for retirement. Your bonus could be the perfect seed money for a significant life goal that’s 5-10 years away.

- Down Payment Fund: A bonus can significantly accelerate your path to homeownership.

- New Car Fund: Saving a lump sum now can mean avoiding a high-interest car loan later.

- “Life Happens” Fund: Perhaps it’s for a wedding, a sabbatical, or starting a business.

For these medium-term goals, you might place the money in a more conservative investment than a pure stock fund, or simply in a high-yield savings account where it can earn a competitive interest rate without market risk.

4. Invest in Yourself: The Highest Possible ROI

Sometimes the investment with the highest return isn’t in the market at all—it’s in you. Your skills and knowledge are your greatest assets and your primary wealth-building tool. Consider using your bonus to:

- Earn a Professional Certification: A credential in your field can directly lead to a higher salary.

- Master a New Skill: Take a course in data analysis, coding, digital marketing, or another high-demand area.

- Hire a Career Coach: A few sessions could unlock a promotion or a more fulfilling career path.

The long-term financial impact of a significant salary increase will likely dwarf the returns from a single market investment.

5. The Hybrid Approach: A Balanced Strategy

Who says you have to choose just one? The “all or nothing” mindset can lead to paralysis. A balanced approach can often be the most sustainable.

The 50/30/20 Bonus Rule: A simple framework to consider.

– 50% to your #1 financial priority (e.g., paying off debt or long-term investing).

– 30% to a secondary goal (e.g., a down payment fund or investing in yourself).

– 20% for guilt-free spending. Enjoy it! This prevents burnout and makes the saving and investing portion feel like a victory, not a sacrifice.

This approach satisfies your desire for immediate reward while ensuring the bulk of your bonus goes toward building a stronger financial future.

Conclusion: From Windfall to Wealth

Your year-end bonus is more than just extra cash; it’s a crossroads. One path leads to the short-lived pleasure of consumption, the other to the enduring satisfaction of building wealth and security. By viewing it as a strategic opportunity—to erase debt, to fuel your retirement engine, to plant seeds for future growth—you transform a simple bonus into a pivotal moment in your financial journey.

The smartest decision is rarely the most exciting one in the moment, but it’s the one that buys you freedom and options in the future. This year, give yourself the gift of a deliberate choice. Turn your hard-earned bonus into the foundation of your future success.

This article is for informational purposes only and should not be considered financial advice.