Is Your Portfolio Ready for 2026? How to Hedge Against Interest Rate Volatility

The financial landscape is bracing for a pivotal year. As we look towards 2026, the whispers from central banks have grown into a discernible hum, signaling a new chapter in monetary policy. For the experienced investor, this isn’t a time for panic, but for precision. If you’re asking how to adjust your investment portfolio for 2026’s interest rates, you are already ahead of the curve. This isn’t just about defense; it’s about strategically positioning for the opportunities that volatility inevitably creates.

The era of predictable, near-zero rates is a fading memory. The coming shifts will test every portfolio, rewarding the prepared and penalizing the complacent. This guide will provide actionable strategies to not only weather the storm but to harness its power, focusing on sophisticated yet practical adjustments to your bond and equity allocations.

The 2026 Rate Conundrum: Why This Time is Different

Before we adjust our sails, we must understand the winds. The 2026 interest rate environment isn’t a simple replay of past tightening or easing cycles. It’s a complex interplay of post-pandemic economic normalization, persistent inflationary pressures, and a global deleveraging. Statements from the Federal Reserve and the European Central Bank suggest a delicate balancing act: taming inflation without stifling growth. This creates a unique form of volatility.

So, how do Fed rates impact stocks and bonds? The fundamental principle remains unchanged: the price of money—the interest rate—is the gravitational force for all asset valuations.

“Think of the bond market as a seesaw. On one end sits bond prices, and on the other, interest rates. When rates go up, prices go down. The longer your bond’s maturity, the further out you are on that seesaw, and the more you feel the swing.”

This inverse relationship is the central challenge for investors heavily weighted in long-duration fixed-income assets. A portfolio that was a bastion of stability for the last decade could become a source of unexpected capital loss. But within this challenge lies our first strategic imperative.

Strategy 1: De-Risking Your Bond Allocation with Laddering

The most immediate threat is to the fixed-income portion of your portfolio. Simply selling off bonds is a blunt instrument. A more elegant solution is the bond ladder strategy for 2026. This isn’t a market timing trick; it’s a structural fortification.

Imagine a staircase instead of a seesaw. A bond ladder involves dividing your fixed-income investment into several “rungs,” each representing a bond with a different, staggered maturity date. For example, if you have $100,000 to invest, you might build a five-year ladder like this:

- $20,000 in a 1-year bond

- $20,000 in a 2-year bond

- $20,000 in a 3-year bond

- $20,000 in a 4-year bond

- $20,000 in a 5-year bond

As each year passes, the 1-year bond matures, providing you with liquidity. You can then reinvest that capital into a new 5-year bond at the top of your ladder, likely capturing the new, higher interest rates. This strategy accomplishes two critical goals:

- Reduces Interest Rate Risk: You avoid having all your capital locked into long-duration bonds that would lose significant value in a rising rate environment.

- Improves Liquidity and Adaptability: A portion of your capital becomes available each year, allowing you to adapt to changing market conditions or personal financial needs without selling assets at a loss.

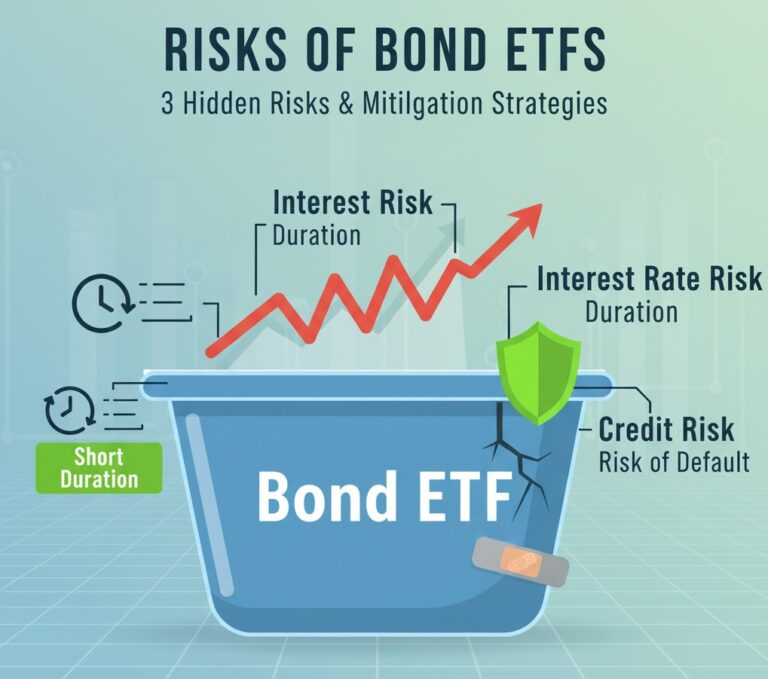

For those who prefer a more hands-off approach, many bond ETFs offer a similar risk-management profile. Consider exploring ETFs focused on short or ultra-short duration bonds.

Strategy 2: Equity Rotation—Finding the Best Sectors for Rising Rates

On the equity side, a rising rate environment is not a uniform headwind. It creates distinct winners and losers. A rising interest rate investment strategy for equities is about rotating capital into sectors that have historically demonstrated resilience or even benefited from higher rates.

- Financials (Banks, Insurance): This is the most direct beneficiary. As rates rise, banks can increase their net interest margin—the spread between what they pay for deposits and what they earn on loans.

- Industrials and Materials: These sectors often thrive in an inflationary environment that accompanies rising rates, as they can pass on higher input costs and benefit from strong economic demand.

- Value Stocks over Growth Stocks: High-growth technology companies, whose valuations are often based on distant future earnings, are particularly sensitive to rate hikes. Higher rates mean future cash flows are discounted more heavily, making them less attractive. Value stocks, with strong current cash flows, tend to perform better.

This doesn’t mean abandoning growth sectors entirely, but it does suggest a strategic rebalancing. Review your equity allocation and consider trimming positions in high-multiple tech stocks in favor of quality value names and financials.

Putting It All Together: Portfolio Allocation by Risk Tolerance for 2026

The right strategy is deeply personal. Here are three sample portfolio adjustments based on different risk profiles. These are not prescriptions, but frameworks for discussion with a financial advisor.

Strategic Allocation Adjustments for 2026

Conservative Investor:

- Current (Sample): 30% Equities, 70% Bonds (heavy in long-duration)

- Proposed 2026 Allocation: 30% Equities (tilting to Value/Financials), 60% Bonds (structured as a 1-5 year ladder), 10% Cash/Cash Equivalents (to capture opportunities).

Moderate Investor:

- Current (Sample): 60% Equities, 40% Bonds

- Proposed 2026 Allocation: 60% Equities (reducing high-growth exposure, increasing Industrials/Financials), 40% Bonds (mix of short/intermediate duration, possibly via ETFs).

Aggressive Investor:

- Current (Sample): 80% Equities, 20% Bonds

- Proposed 2026 Allocation: 80% Equities (maintaining core growth but adding cyclical/value hedges), 20% Bonds (focused on short-duration and inflation-protected securities like TIPS).

Conclusion: From Volatility to Opportunity

Navigating the 2026 interest rate environment is not about making radical, all-or-nothing bets. It is about making a series of deliberate, incremental adjustments that realign your portfolio with the new economic reality. By restructuring your bond holdings through laddering and strategically rotating your equity exposure towards resilient sectors, you transform volatility from a threat into a source of opportunity.

The financial tides are turning, but for the prepared investor, this is not a cause for fear. It is a call to action. Review your holdings, stress-test your assumptions, and position yourself not just to survive the coming volatility, but to thrive in it.

This article is for informational purposes only and should not be considered financial advice.